Great companies can be built serving consumers or enterprises. But there’s a different risk-reward return profile. I recently took a step back to look at the data along with my colleagues and awesome thought partners Kate Walker, Alexandra Sukin, and Jeremy Levine. We reviewed all the VC-backed public listings on the NYSE & Nasdaq worth >$1B and all VC-backed M&A exits worth >$500m since 2001. See footnote for methodology.

Here are some of the findings:

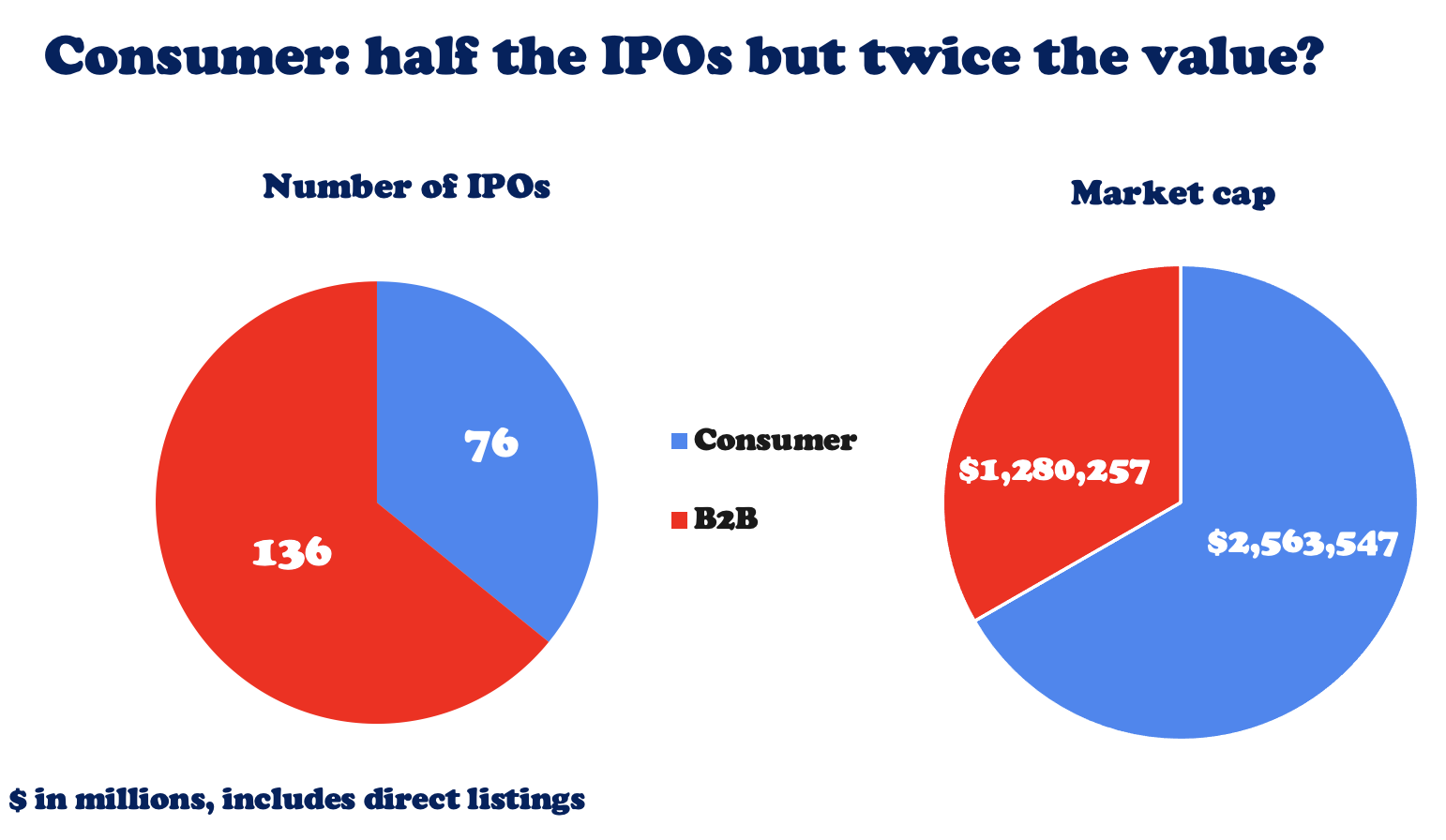

There are 76 consumer and 136 B2B publicly traded companies in the data set. The current market cap of the consumer companies is 2x greater than the B2B companies despite roughly half the listings.

There is an extreme power law:

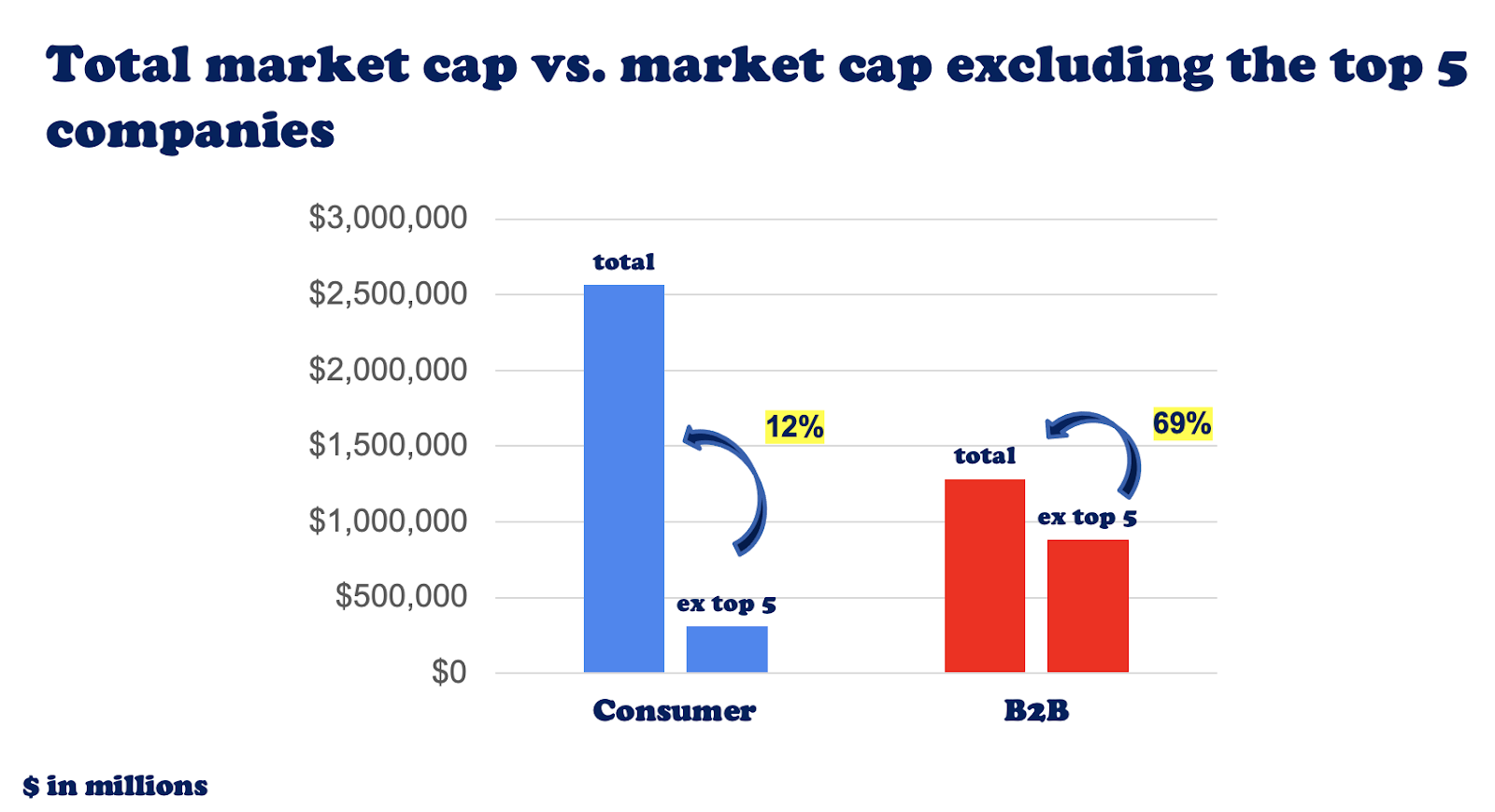

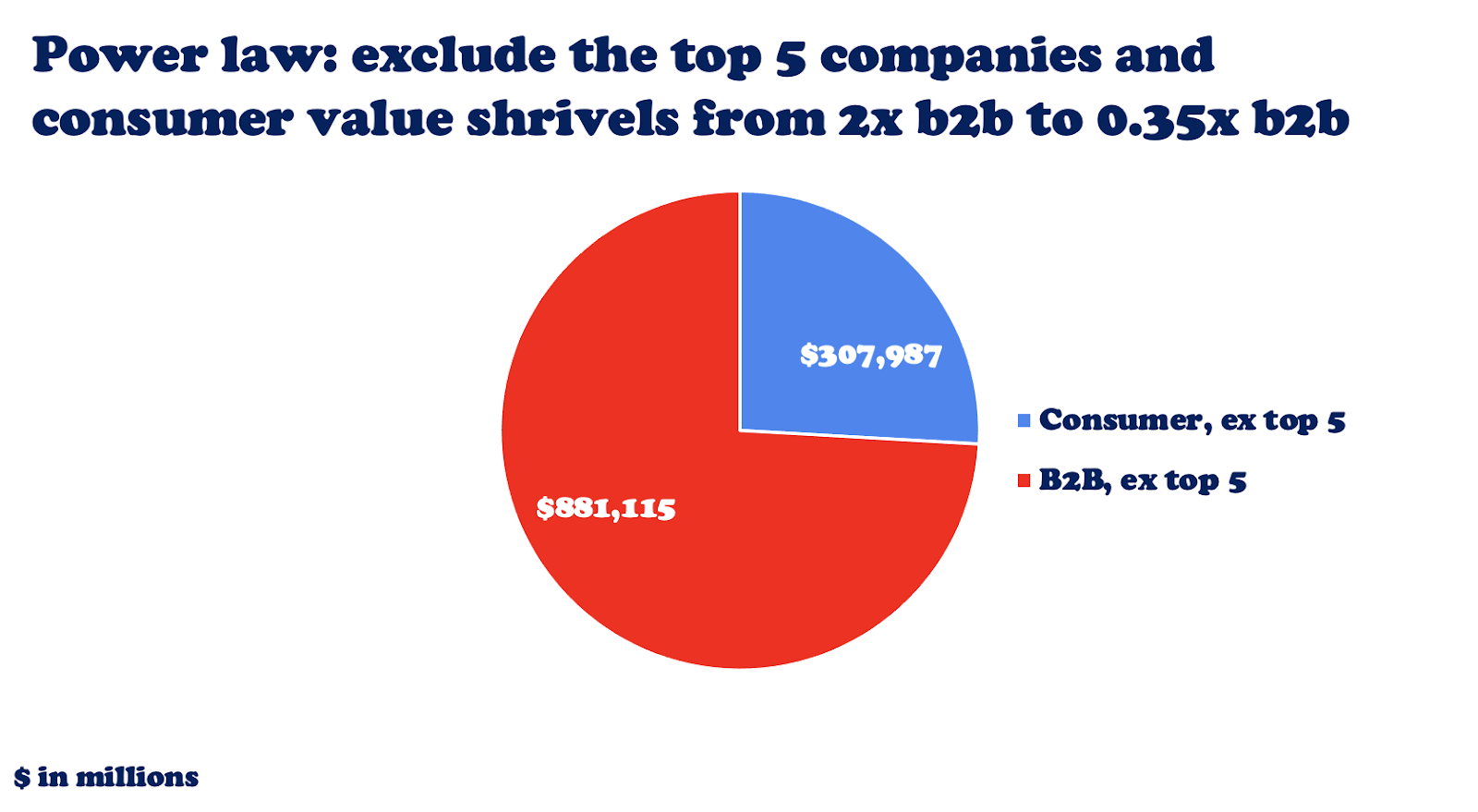

Remove the top five consumer and B2B names, and the current market value of the consumer companies drops from 2x to just 1/3rd the size of B2B.

In other words, the market cap of B2B companies is nearly three times larger than consumer if you remove the top five companies in each sector.

Consumer market cap is left with just 12% of its total current value when the top five consumer internet companies are excluded. The enterprise market cap shrinks to 69% of its total when the top five enterprise companies are excluded.

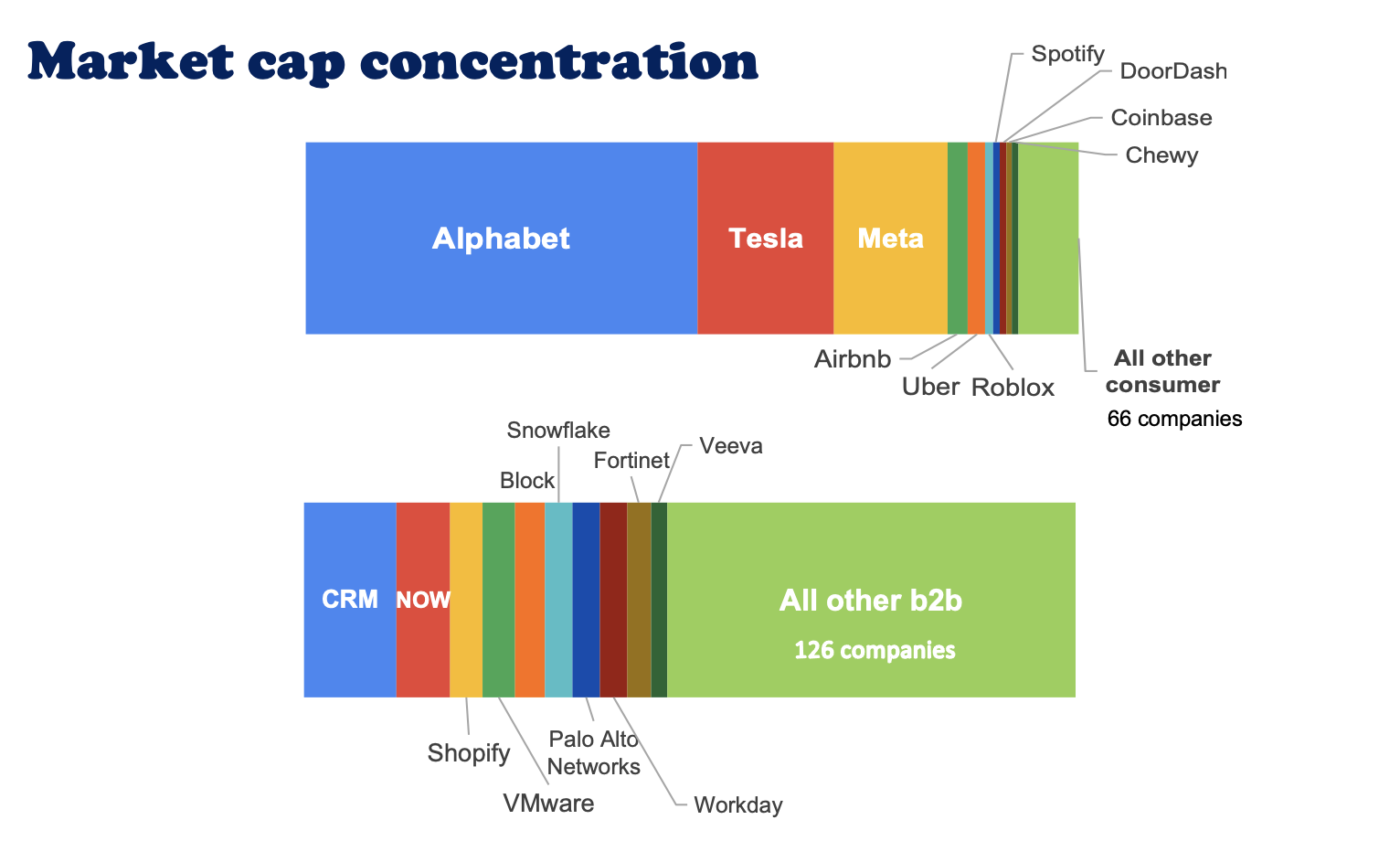

Google, the top consumer company, represents 52% of the current consumer value. The top five companies represent 88% of its value: Alphabet, Tesla, Meta, Airbnb, and Uber.

Salesforce, the top B2B company, represents 11% of current B2B value. The top five companies are 31% of its value: Salesforce, ServiceNow, Shopify, VMWare, and Block.

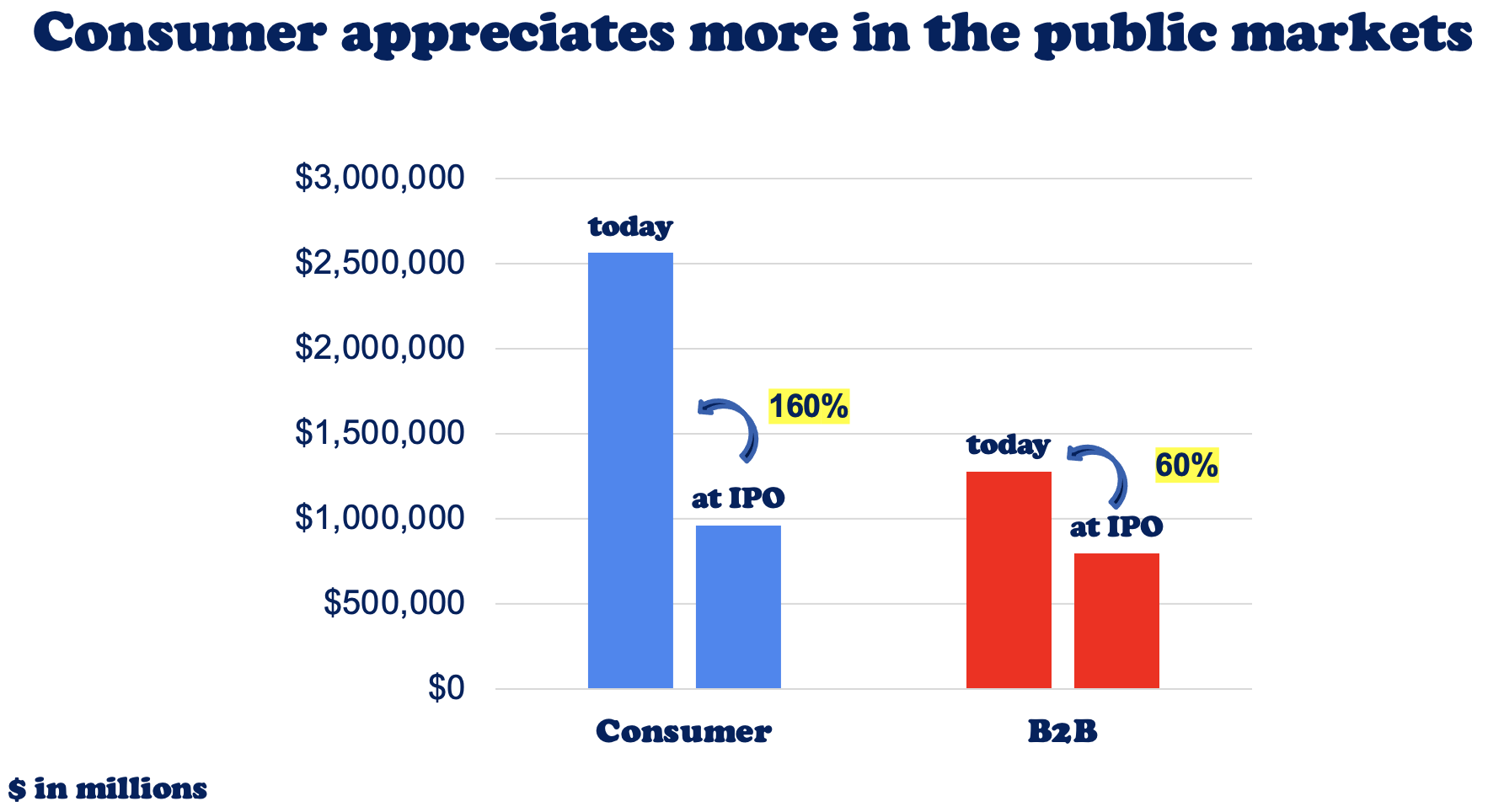

How do consumer internet companies fare post IPO?

Post-IPO, consumer companies appreciated 160% on average, compared to 60% for enterprise companies.

But the market cap of consumer internet companies depreciates by 44% (!) when the top five companies are excluded. In contrast, B2B still appreciates by 40% when the top five are excluded.

It is surprising that the average consumer internet company lost value post IPO whereas enterprise companies fared far better. I have two hypotheses for why:

First, this analysis only reflects a moment in time, so it may not be indicative of the long-term picture. The 2020-2021 market exuberance may be one factor driving this depreciation. Many large consumer companies like Doordash, Airbnb, Coinbase, Roblox, and Rivian went public in this period and were worth $350b+ at listing, but as of late January just ~$150b.

These market dynamics were also at play for the B2B companies that went public in 2020-2021. But the larger number of public B2B companies, and greater number that went public before this exuberant period, yields a blended average of 40% appreciation since IPO.

Second, as web 2.0 matures, it has become increasingly difficult for startup consumer internet companies to succeed. Mega platforms such as Meta, Alphabet, Apple, and Amazon control most consumer internet distribution. This is one reason VCs drool over platform shifts or powerful technology advances that create opportunity. For example, ChatGPT reached 100 million monthly active users just two months post launch thanks to “magical” technology that disrupt the status quo. And while there are many distribution tactics that can overcome this environment, it is harder today than it was 10 or 15 years ago.

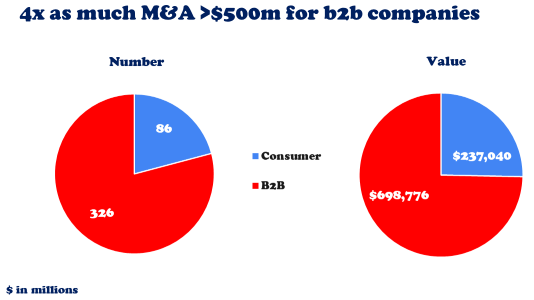

What about M&A?

There is 4x the M&A >$500m for enterprise companies. The fewer consumer internet acquisitions is partially attributable to the other side of the “mega platform” coin: antitrust scrutiny.

The largest consumer internet CEOs have all found themselves in front of Congress in recent years. Zuck had to take the stand to defend Meta’s acquisition of VR fitness app Within, rumored to be worth just ~0.1% of its market cap, yet scrutinized in a lengthy process.

A few other takeaways:

- In consumer, second place gets steak knives and third place is fired. The winners have long runways and big upside. Growth investors better have conviction they are backing the winner.

- Second place ain’t so bad in enterprise. The largest B2B company, Salesforce, has just ~23% CRM market share. By contrast, Uber claims 70%+ of the rideshare market vs. Lyft and boasts a 15x+ higher market cap.

- The sector indexing strategy strikes me as especially foolish in consumer. Missing the one can mean missing it all. Mistakes of omission are costly.

- No single VC led the Series A of more than 2 of the top 5 consumer outcomes. But it only takes that one to be iconic.

- Consumer may appear “hit driven” but most big consumer exits were beneficiaries of major market shifts – early internet, mobile, or recently AI, crypto, and clean energy, with innovative products and moats.

- Network effects win. Most of the big consumer exits since 2001 have network effects as moats.

- Twice as hard but twice as fun? The upside in consumer is greater, but it has been ~2.5x harder to generate VC returns. There were 21 consumer vs 51 b2b public names >$5B, or 38 consumer vs. 92 b2b public names >$2B.

- The concentrated market value + antitrust regulation is making consumer M&A harder. By contrast, B2B M&A is expanding thanks to PE buyers.

Will this change where I invest?

Probably not. While history rhymes, this is backwards looking. And I’m looking to the future. I want to be involved with impactful businesses that transform how we live. I love consumer investing. But I consider myself a “roadmap driven generalist” (more on that in a future post). If I have a thesis on a trend or space and have conviction in the related opportunities – consumer, B2B, or otherwise, I am all in.

–—

Methodology and source: data pulled from Capital IQ in late January 2023, based on VC-backed companies since 2001 with NYSE & Nasdaq IPO, direct listing or acquisition market caps greater than $500M. M&A activity outside of North America and Europe was excluded for the purposes of this study.

Companies were manually reviewed and tagged for consumer internet vs. B2B, so this is subject to human error. Damn humans! All other VC-backed categories including deep tech, semis, telco, biotech, as well as PE owned companies that were not previously VC-backed. Fintech is included and bucketed as either consumer or B2B.

For those asking “where are Apple and Amazon”? They are missing because they went public in 1980 and 1997, respectively. As per above this is based on VC-backed exits that occurred since 2001 and fit the criteria above.